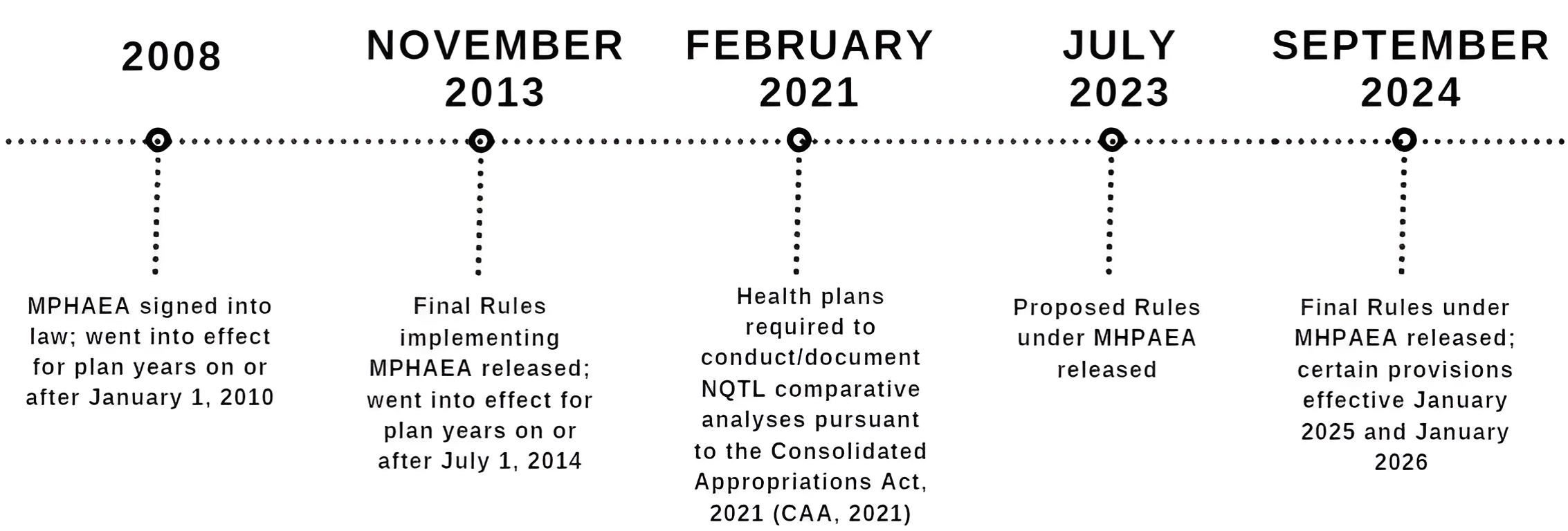

The wait is over now that the Department of Health and Human Services, the Department of Labor, and the Department of the Treasury (collectively, the “Departments”) released the Mental Health Parity and Addiction Equity Act (MHPAEA) Final Rules (“Final Rules” hereinafter) on September 9, 2024. These much-anticipated Final Rules arrive on the heels of proposed rules released in July 2023[1] and after the Departments reviewed almost 10,000 comments submitted by interested parties.[2]

The newly released Final Rules, along with the previously proposed rules, are direct responses to the mental health and substance abuse crisis exacerbated by the COVID-19 pandemic and the May 2023 Surgeon General advisory on loneliness and isolation. These Final Rules amend existing provisions under MHPAEA and clarify and expand requirements under the Consolidated Appropriations Act, 2021 (“CAA, 2021”). The Departments hope the Final Rules will improve overall mental health and substance abuse disorder (MH/SUD) benefits offered in group (and individual) health plans.

For the sake of brevity, this article will summarize the extensive guidance provided under the Final Rules, as well as highlight key details, dates, and action items most relevant to employer-sponsored group health plans.

Read on for more information.

MHPAEA Background

MHPAEA prevents group health plans providing MH/SUD benefits from imposing limits on those benefits that are more stringent than limits imposed on medical/surgical (M/S) benefits. This generally means that any of the following requirements imposed on a plan’s MH/SUD benefits cannot be more restrictive than those applied to the plan’s M/S benefits:

- Financial requirements — such as deductibles, co-payments, coinsurance, and out-of-pocket maximums

- Quantitative treatment limitations — such as number of treatments, visits, or days of coverage

- Non-quantitative treatment limitations (NQTLs) — such as prior authorization requirements, step therapy, and standards for provider admission to participate in a network, including methodologies for determining reimbursement rates.

NQTLs are generally non-numerical requirements that limit the scope or duration of benefits.

Plans Subject to MHPAEA

MHPAEA requirements generally apply to self-funded, fully insured, grandfathered, and non-grandfathered plans that offer MH/SUD benefits. Some group health plans are exempt from MHPAEA requirements, including:

- Self-funded plans sponsored by employers with 50 or fewer employees;

- Plans offering only excepted benefits (e.g., vision-only or dental-only coverage); and

- Retiree-only plans.

Fully insured employer plans with 50 or fewer employers are generally required to comply with MHPAEA by satisfying the essential health benefit (also known as “EHB”) requirements of the ACA.

CAA, 2021

The CAA, 2021, amended MHPAEA, to expressly require group health plans subject to MHPAEA to conduct and document comparative analyses of the design and application of NQTLs, and provide this analysis to the Departments (or an applicable state authority) and participants upon request. This NQTL comparative analysis requirement went into effect on February 10, 2021 and currently remains in effect for group health plans.

MPHAEA Timeline

MHPAEA Final Rule Highlights

Highlights of the Final Rule relevant to employers sponsoring group health plans include the following:

- Key Terms Definitions: The Final Rules revise the definitions of certain key terms (such as medical/surgical benefits,” “mental health benefits,” and “substance use disorder benefits,” among others) by removing a reference to state law and guidelines. Importantly, a plan’s definition of a MH/SUD condition is required to align with the most current version of the International Classification of Diseases (ICD) or the Diagnostic and Statistical Manual of Mental Disorders (DSM).

- No More Restrictive Standard: Plans cannot use NQTLs that are more restrictive, as written or in operation, than the predominant NQTLs applied to substantially all M/S benefits in the same benefits classification. Plans must consider processes, strategies, evidentiary standards, and other factors used to design and apply the NQTL. For this purpose, plans are required to meet two sets of requirements:

- Design and application requirements: This element generally refers to a prohibition on the use of discriminatory factors and evidentiary standards to design an NQTL to be imposed on MH/SUD benefits. A factor or evidentiary standard is discriminatory if the information, evidence, sources, or standards on which it is based are biased or not objective in a manner that discriminates against MH/SUD benefits as compared to M/S benefits.

For clarity, independent professional medical or clinical standards are generally considered nonbiased and objective.

Much to the relief of all impacted stakeholders, the Final Rules do not require application of the mathematical tests to determine “substantially all” and “predominant” as had been set forth in the proposed rules.

- Relevant data evaluation requirements: Plans are required to collect and evaluate relevant outcomes data in a manner reasonably designed to assess the impact of each NQTL on relevant outcomes related to access to MH/SUD benefits and M/S benefits, and then carefully consider the impact. If the relevant data suggests that the NQTL contributes to material differences in access to MH/SUD benefits as compared to M/S benefits in the same benefits classification, such differences will be considered a strong indicator that the plan violates MHPAEA. The plan must take reasonable action to address these material differences, document these actions, and how they mitigate the material differences.

Notably, under this rubric of data evaluation, the Final Rules modify the network composition NQTL, mandating plans to collect and evaluate data in a manner reasonably designed to assess the aggregate impact of all such NQTLs on access to MH/SUD disorder benefits and M/S benefits, rather than evaluating relevant data for each NQTL separately (which is generally required under the Final Rules), to determine if there is a material difference in access.Acknowledging the concerns of various comments with respect to the network composition NQTL and MH/SUD provider shortages, the preamble to the Final Rules states “that certain outcomes measures, such as high out-of-network utilization for MH/SUD benefits as compared to M/S benefits, “may not necessarily represent a per se violation of MHPAEA.”[3]

The Final Rules attempt to alleviate this provider shortage concern by listing steps that group health plans, working in conjunction with their plan service providers, could take, including:

- Conducting recruiting and outreach efforts to encourage more MH/SUD providers, including known out-of-network providers, to join the plan’s network by:

- increasing compensation and

- streamlining credentialing processes.

- Expanding telehealth arrangements, especially in areas with shortages of MH/SUD providers.

- Conducting outreach and assistance efforts directly to plan participants to assist them with locating in-network MH/SUD providers, including improving provider directory accuracy and reliability.

Additionally, the Final Rules provide guidance for the limited circumstances where no relevant data exists relating to an NQTL, such as exclusions related to experimental or investigative treatment.[4] In these instances, the plan must “include in its comparative analysis a reasoned justification as to the basis for its conclusion that there are no data that can reasonably assess the NQTL’s impact, why the nature of the NQTL prevents the plan or issuer from reasonably measuring its impact, an explanation of what data was considered and rejected, and documentation of any additional safeguards or protocols used to ensure that the NQTL complies with MHPAEA.”

Ultimately, the Final Rules do provide flexibility for plans determine what should data be collected and evaluated, as appropriate, since the relevant data for any given NQTL will depend on the facts and circumstances.

- Conducting recruiting and outreach efforts to encourage more MH/SUD providers, including known out-of-network providers, to join the plan’s network by:

- Design and application requirements: This element generally refers to a prohibition on the use of discriminatory factors and evidentiary standards to design an NQTL to be imposed on MH/SUD benefits. A factor or evidentiary standard is discriminatory if the information, evidence, sources, or standards on which it is based are biased or not objective in a manner that discriminates against MH/SUD benefits as compared to M/S benefits.

- Meaningful Benefits: Plans that provide any benefits for MH/SUD conditions in any benefits classification must provide meaningful benefits for that condition in every classification in which meaningful M/S benefits are provided. Meaningful benefits are determined in comparison to the benefits provided for M/S conditions in the same classification.

- Meaningful benefits require coverage of a “core treatment” for a MH/SUD condition or disorder in each classification in which the plan or coverage provides benefits for a core treatment for one or more M/S conditions or procedures. Core treatment is generally defined as “standard treatment or course of treatment, therapy, service, or intervention indicated by generally recognized independent standards of current medical practice.”

- Classifications refer to the following six categories below:

- In-network outpatient

- In-network inpatient

- Out-of-network outpatient

- Out-of-network inpatient

- Emergency care

- Prescription drugs

- NQTL Comparative Analysis Requirement: The Final Rules also clarify the content requirements for the written NQTL comparative analysis requirement, including, for example, evaluating standards related to network composition, out-of-network reimbursement rates, and medical management and prior authorization NQTLs.

The Final Rules outline the six elements required to be included in the written NQTL comparative analysis (in addition to the requirements to include a written list of all NQTLs imposed under the plan), which are summarized below:

- a description of the NQTL, including identification of benefits subject to the NQTL;

- identification and definition of the factors and evidentiary standards used to design or apply the NQTL;

- a description of how factors are used in the design or application of the NQTL;

- a demonstration of comparability and stringency, as written;

- a demonstration of comparability and stringency, in operation, including the required data, evaluation of that data, explanation of any material differences in access, and description of reasonable actions taken to address such differences; and

- findings and conclusions.

- Sunset of MHPAEA Opt-Out For Specific Plans: The Final Rules implement the sunset provision for self-funded non-federal governmental plan elections to opt out of compliance with MHPAEA. Click here for an article with more information.

ERISA Fiduciary Certification

For group health plans subject to ERISA[5], the Final Rules also require the comparative analysis to include a certification by one or more named plan fiduciaries confirming they have engaged in a prudent process to select and monitor their plan service providers performing and documenting their NQTL comparative analysis. This requirement will have significant implications for employer group health plan sponsors since a named plan fiduciary will have to be familiar with and understand the NQTL analysis, as well as prudently select and monitor the service that completes the analysis.

Much to the relief of ERISA group health plan sponsors, the Final Rules removed a proposed provision requiring a plan fiduciary to certify that the NQTL comparative analysis complies with regulatory content requirements.

Illustrative Examples

Since these Final Rules are very extensive and can be difficult to digest, the Departments provided illustrative examples providing practical, real-world context for employers sponsoring group health plans in their compliance efforts. Several of these illustrative examples are detailed below:

A plan covers treatment for autism spectrum disorder (ASD), a MH condition, and covers outpatient, out-of-network developmental screenings for ASD but excludes all other benefits for outpatient treatment for ASD, including applied behavior analysis (ABA) therapy, when provided on an out-of-network basis. The plan generally covers the full range of outpatient treatments (including core treatments) and treatment settings for M/S procedures when provided on an out-of-network basis. Under the generally recognized independent standards of current medical practice consulted by the plan, developmental screenings alone do not constitute a core treatment for ASD.

Result: This plan feature violates MHPAEA since although it only covers developmental screenings, it does not cover a core treatment for ASD in the classification. Because the plan generally covers the full range of M/S benefits including a core treatment for one or more M/S procedures in the classification, it fails to provide meaningful benefits for treatment of ASD in the classification.

NOTE: A subsequent example contains the same facts as above but the plan is an HMO that does not the cover the full-range of M/S benefits, including core treatment for any M/S procedures in the outpatient, out-of-network classification. This particular plan design does not violate MHPAEA because the plan does not provide meaningful benefits, including for a core treatment for any M/S procedure in the outpatient, out-of-network classification (except under the No Surprises Act). As such, the plan is not required to provide meaningful benefits for any mental health conditions or substance use disorders in that classification.

A plan provides extensive benefits, including for core treatments for many M/S procedures in the outpatient, in-network classification, including nutrition counseling for diabetes and obesity. The plan also generally covers diagnosis and treatment for eating disorders, which are MH conditions, including coverage for nutrition counseling to treat eating disorders in the outpatient, in-network classification. Nutrition counseling is a core treatment for eating disorders, in accordance with generally recognized independent standards of current medical practice consulted by the plan.

Result: This plan feature is in compliance with MHPAEA since the coverage of diagnosis and treatment for eating disorders, including nutrition counseling, in the outpatient, in-network classification results in the plan providing meaningful benefits for the treatment of eating disorders in the classification, as determined in comparison to the benefits provided for M/S procedures in the classification.

A plan provides extensive benefits for the core treatments for many M/S procedures in the outpatient, in-network and prescription drug classifications. The plan provides coverage for diagnosis and treatment for opioid use disorder, a substance use disorder, in the outpatient, in-network classification, by covering counseling and behavioral therapies and, in the prescription drug classification, by covering medications to treat opioid use disorder (MOUD). Counseling and behavioral therapies and MOUD, in combination, are one of the core treatments for opioid use disorder, in accordance with generally recognized independent standards of current medical practice consulted by the plan.

Result: This plan feature is in compliance with MHPAEA since the coverage of counseling and behavioral therapies and MOUD, in combination, in the outpatient, in-network classification and prescription drug classification, respectively, results in the plan providing meaningful benefits for the treatment of opioid use disorder in the outpatient, in-network and prescription drug classifications.

A plan generally covers inpatient, in-network and inpatient, out-of-network treatment without any limitations on setting, including skilled nursing facilities and rehabilitation hospitals, provided other medical necessity standards are satisfied. The plan has an exclusion for treatment at residential facilities, which the plan defines as an inpatient benefit for MH/SUD benefits. This exclusion was not generated through any broader NQTL (such as medical necessity or other clinical guidelines).

Result: This plan feature violates MHPAEA since the exclusion of treatment at residential facilities is a separate NQTL applicable only to MH/SUD benefits in the inpatient, in-network and inpatient, out-of-network classifications because the plan does not apply a comparable exclusion for M/S benefits in the same classification.

An employer maintains both a major medical plan and an employee assistance program (EAP). The EAP provides, among other benefits, a limited number of MH/SUD counseling sessions, which, together with other benefits provided by the EAP, are not significant benefits in the nature of medical care. Participants are eligible for MH/SUD benefits under the major medical plan only after exhausting the counseling sessions provided by the EAP. No similar exhaustion requirement applies with respect to M/S benefits provided under the major medical plan.

Result: This plan design violates MHPAEA since the MH/SUD EAP limitation does not apply also to M/S benefits. Also, the EAP here would not qualify as an “excepted benefit” under other Departmental regulations since plan participants must exhaust their EAP benefits before using the benefits under the major medical plan.

Department of Labor (DOL) Request to Review NQTL Comparative Analysis

The Final Rules clarify the steps and (relatively tight) timelines that the DOL will generally follow to request and review an ERISA-covered group health plan’s NQTL comparative analysis:

- Upon request, employers sponsoring covered group health plans must submit their NQTL comparative analysis to the DOL within 10 business days.

- If the comparative analysis is found to be insufficient, the DOL will specify the additional information necessary, which must be submitted to the DOL within 10 business days.

- If the DOL makes an initial determination of noncompliance, the DOL will give the plan sponsor 45 calendar days to make corrections and submit additional comparative analyses.

- If the DOL makes a final determination of noncompliance, the plan must issue a notice to all participants and beneficiaries within 7 business days that the plan is not in compliance. The notice must satisfy certain content requirements:

- A notice with prescribed language outlined in the Final Rules must be provided to the DOL as well as applicable plan service providers and fiduciaries.

- Moreover, the DOL could direct the plan sponsor to stop imposing the noncompliant NQTL until it demonstrates compliance to the DOL or takes appropriate action to remedy the violation.

Additionally, group health plans are required to provide a copy of their NQTL comparative analysis to plan participants upon request within 30 days, in accordance with ERISA’s disclosure rules.

Final Rules Effective Dates

The MPHAEA Final Rules generally become effective for plan years beginning on or after January 1, 2025, including the new fiduciary certification for ERISA group health plans.

However, the following provisions within the Final Rules apply on the first day of the first plan year beginning on or after January 1, 2026:

- meaningful benefits standard,

- the prohibition on discriminatory factors and evidentiary standards,

- the relevant data evaluation requirements, and

- the revised NQTL comparative analyses requirements.

Key Takeaways & Action Items for Group Health Plans

As mentioned earlier, these Final Rules are extensive, dense, and can be complex to comprehend. As such, many, if not most, employers sponsoring group health plans will not need to become experts in the nuances and intricacies of these Final Rules.

However, group health plans should become familiar with the Final Rules in light of the fiduciary certification requirement. The Final Rules also provide valuable insight into the Departments’ enforcement priorities and efforts in this space. MHPAEA compliance continues to be a top enforcement priority for the Departments, as evidenced in their MHPAEA Comparative Analysis Report to Congress, July 2023.

On a related note, certain provisions of these final rules could be susceptible to challenges in light of the recent Supreme Court ruling in Loper Bright, overruling the Chevron deference with respect to federal agencies’ regulations. Consequently, the saga of MHPAEA regulations and general compliance will likely continue.

In the meantime, most group health plans are still required to comply with the current CAA, 2021, requirement to conduct and document their NQTL comparative analyses. As plans begin entering renewal season, along with the release of the Final Rules, group health plan sponsors are encouraged to proactively start their compliance efforts now.

As a result, group health plans are advised to start working with their plan service providers (including carriers, third-party administrators (TPAs), pharmacy benefit managers (PBMs), managed behavioral health organizations and/or legal counsel) to:

- Identify and remove any problematic plan features or other plan design concerns that might run afoul of MHPAEA and/or the Final Rules, and

- Conduct and document the required NQTL comparative analyses:

- Fully Insured Plans: Employers sponsoring fully insured plans will rely on their health plan carriers to comply with these Final Rules, as confirmed by the Departments in the Final Rules preamble.[6]

- Self-Funded Plans (including Level-Funded Plans): Employers sponsoring self-funded (and level-funded) plans are directly responsible for complying with the Final Rules. On a practical level, these plans’ service providers are “best situated” to conduct and document the required NQTL comparative analyses, and “to provide the analyses in an efficient and cost-effective manner, helping to reduce the compliance burden,” as echoed in the Final Rules preamble.[7]

Remarkably, the preamble contains specific commentary detailing the DOL’s expectation for plan service providers to support their plan sponsor clients in MHPAEA compliance efforts, including conducting and documenting required NQTL analyses. As confirmed in the preamble, “DOL also underscores its commitment to holding fiduciaries of ERISA-covered group health plans liable through existing means and working with all relevant entities, including service providers, to effectuate MHPAEA compliance.”[8]

The preamble language continues on to state, “Where NQTL violations are identified in a plan or coverage, DOL generally examines the role that each of the plan’s or issuer’s service providers have in the design and administration of each NQTL to ascertain whether any of the service providers play a similar role serving other plans or issuers that might have the same violations, and seeks to bring them into compliance. Where necessary, DOL determines who is a fiduciary under ERISA and what additional enforcement actions are necessary. DOL notes that determinations of fiduciary liability are often based on the facts and circumstances specific to individual cases, but to the extent a TPA exercises discretionary authority or discretionary responsibility in the administration of an ERISA-covered health plan, DOL generally considers them to be fiduciaries.”[9]

The Departments even recommend group health plans to expressly contract for MHPAEA compliance (including completion of NQTL comparative analyses) in their agreements with their plan service providers as a “best practice.”[10]

Finally, the Departments proclaim their intention, in the Final Rules, to publish additional guidance and compliance support for impacted stakeholders, including employers sponsoring group health plans. The Departments are also planning to update the 2020 MHPAEA Self-Compliance Tool to “provide a robust framework and roadmap for plans and issuers to determine which data to collect and evaluate.”[11]

eBen is closely following developments related to the Final Rules and MHPAEA generally, and will provide updates when available. Contact your eBen account team with any questions or contact us directly here.

[2] Interested parties included employee organizations and other plan sponsors, health care providers and facilities, health insurance organizations, consumer and advocacy organizations, third-party administrators, pharmacy benefit managers, and others.

[3] Preamble to MHPAEA Final Rules on Page 115.

[4] These NQTLs might not generally be attached to claims, so plans may not have reliable data on the impact of these excluded services on plan participants.

[5] The Employee Retirement Income Security Act of 1974.

[6] Id. at 260.

[7] Id. at 258.

[8] Id. at 94.

[9] Id. at 94.

[10] Id. at 93.

[11] Id. at 89.

The contents of this article are for general informational purposes only and Risk Strategies Company | eBen makes no representation or warranty of any kind, express or implied, regarding the accuracy or completeness of any information contained herein. Any recommendations contained herein are intended to provide insight based on currently available information for consideration and should be vetted against applicable legal and business needs before application to a specific client.